Vista Gold – 10.6 Million Ounces Of Aussie Gold And Key Takeaways From The New Optimized Feasibility Study At The Mt Todd Project

Fred Earnest, President and CEO of Vista Gold Corp. (NYSE American and TSX: VGZ), joins us for comprehensive update on the revised Resource Estimate, and the new optimized Feasibility Study announced July 29th at their Mt Todd Gold Project. Mt Todd is a ready-to-build development-stage gold deposit located in the Tier-1 mining jurisdiction of Northern Territory, Australia.

Fred reviews the 10.6 million ounces of gold resources in all categories, and the infrastructure and jurisdiction advantages to the working in this area of Australia. We then shifted over to lower capex and key efficiencies outline in the updated 2025 Feasibility Study (“2025 FS”). This new 2025 FS provides a favorable development alternative to Vista’s previous feasibility study completed in 2024 at 50,000 tpd, as it now envisions a 15,000 tonnes per day (“tpd”) mining scenario. This smaller initial project has a much lower capex, and prioritizes higher grade ore being sent to the processing plant, significantly reducing development capital required and operational risks.

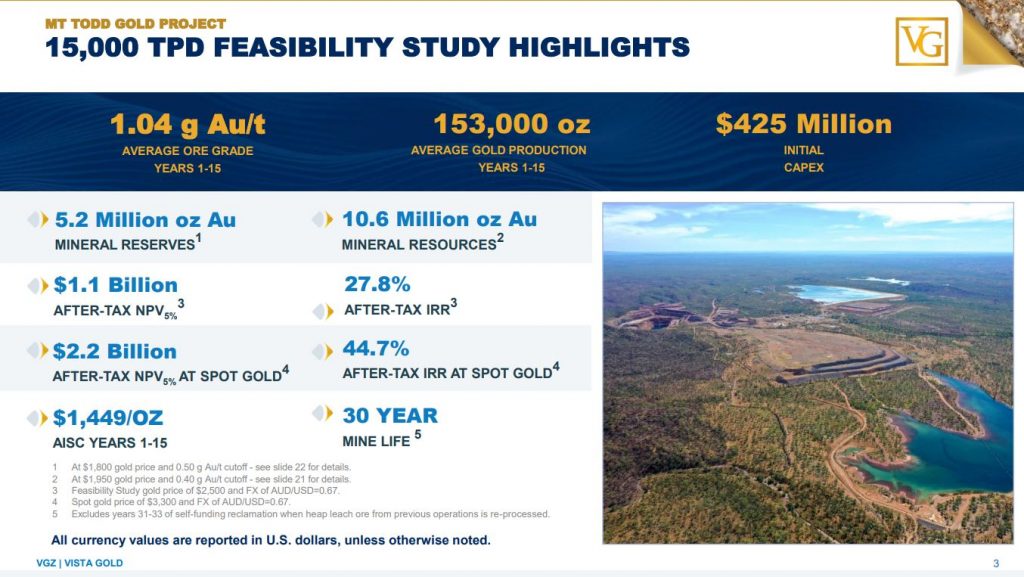

FEASIBILITY STUDY HIGHLIGHTS

- Average annual gold production of 153,000 ounces during years 1-15 and 146,000 over the 30-year life of mine

- Average ore grade of 1.04 grams gold per tonne (“g Au/t”) over the first 15 years of operations and 0.97 g Au/t over the life of mine

- Life of mine average gold recovery of 88.5% from 3-stage crush, single-stage sort, 2-stage grind, and carbon-in-leach (“CIL”) recovery circuit

- Contract mining and third-party power generation reduce capital costs and operational risks

- Future expansion opportunities not evaluated in the Study, but considered in designs and layouts

ROBUST PROJECT ECONOMICS

- After-tax NPV5% of $1.1 billion, IRR of 27.8% and 2.7 year payback at a $2,500 per ounce gold price

- After-tax NPV5% of $2.2 billion, IRR of 44.7% and 1.7 year payback at spot gold price ($3,300 per ounce)

- After-tax free cash flow at a $2,500 gold price of $1.6 billion for first 15 years of commercial operations

- Initial capital requirements of $425 million, a 59% reduction from the 2024 FS

- Capital Efficiency: $93 per ounce (initial capital : total ounces of gold produced)

- All-in Sustaining Cost of $1,449 per oz years 1-15 and $1,499 per oz years 1-30

If you have questions for Fred regarding Vista Gold, then please email those into us at Fleck@kereport.com or Shad@kereport.com

Click here to follow the latest news from Vista Gold Corp

.

.

I bought some HGRAF yesterday as you were selling. At what price are you planning to buy back. I want to buy more. I bought some Vista Gold about 20 years ago and am still waiting for something to happen. Maybe I should sell my Vista and put it into HGRAF…

Hi Bonzo, I buy on the CDN exchange, I am looking to get back in below $1.60. I noticed it seems to have bottomed for now, but any news will shoot this stock much higher. DT

I am watching HydroGraph very closely a lot of people want in and as soon as they start buying back the shorts hit the stock with another attack and down she goes. You must be very careful here. DT

Hi DT, HG is 1.58 in Canada now and I just bought more @ 1.17.

If it falls on news that Bonzo is in, as it surely will, I plan to buy more.

LOL! That’s funny! DT

I got out of HydroGraph yesterday again (fourth time) and am waiting to buy back in. As a trader you must preserve capital. But a story like HydroGraph will draw me back in at some point. DT